If you have ever sat down with a financial advisor, chances are they talked your ear off about compound interest. And they were right to. The earlier money starts growing, the more dramatically it multiplies over time. That principle is at the heart of a new federal program that every parent, grandparent, aunt, and uncle should know about right now, regardless of where you fall politically.

This is not about politics. This is about a real financial opportunity for the children in your life.

What Exactly Is a Trump Account

Trump Accounts are a new type of individual retirement account created for eligible children, established under the Working Families Tax Cuts Act. Parents or guardians can open and manage the account on behalf of their child, and the federal government will make a one-time $1,000 pilot contribution to the account of each eligible child who is a U.S. citizen born on or after January 1, 2025, through December 31, 2028.

Think of it as a baby shower gift from the federal government, except instead of a onesie, it is a financial foundation. This gift is not meant to be unwrapped until your child turns 18, giving the investment time to compound and eventually be put toward life’s biggest milestones, like going to college or buying a house.

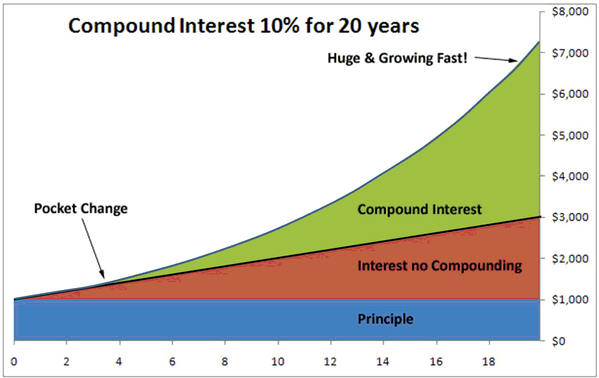

How Much Could $1,000 Actually Grow To

This is where compound interest does its quiet, powerful work, and the numbers are worth sitting with for a moment.

For an account created at birth with the $1,000 seed investment and no other contributions, the Treasury estimates the account could grow to about $6,000 at 18 years old, $15,000 at 27, and $243,000 at 55, assuming an average annual return of about 10.5%.

Now imagine what happens if a family adds to that account along the way. If a family contributes and invests the full $5,000 annually for all 18 years, assuming a 6% annual growth rate, the account could hold around $191,000 in assets by the time the child turns 18. Even if no additional contributions are made after that, by the time the beneficiary reaches age 60, the account could be worth more than $2.2 million.

That is the power of starting early. Every year of growth matters, which is exactly why this program is worth paying attention to now rather than later.

What the Money Can Be Used For

Here is the part that connects directly to homeownership. When your child turns 18, they can use the funds for specific purposes, including paying tuition, starting a business, or making a down payment on a home.

Given how challenging the path to homeownership has become for younger generations, having an account earmarked and growing from birth is a meaningful advantage. The down payment hurdle is one of the biggest barriers first-time buyers face. A Trump Account does not solve that problem overnight, but 18 years of compound growth can make a real dent in it.

Who Can Contribute and How It Works

The $1,000 from the federal government is the floor, not the ceiling. Families can contribute up to $5,000 per year, and employers can add another $2,500 pre-tax through employer cafeteria plans, effectively creating a new pre-tax savings vehicle for families. Charitable organizations and government entities can also make contributions that do not count against the $5,000 family limit.

Several major companies have already pledged to match employee contributions to Trump Accounts, including JPMorgan Chase, IBM, and Comcast. And Michael Dell and his wife Susan Dell announced a $6.25 billion donation to fund accounts for 25 million children, contributing $250 per account for children under 10 in lower-income zip codes.

The investments inside the account are intentionally simple. Funds must be invested in low-cost index mutual funds or ETFs focused primarily on U.S. companies, with an expense ratio cap of 0.10%, meaning fees are kept extremely low to maximize long-term growth.

How to Get Started

The process to claim the $1,000 seed deposit is straightforward, but there is a timeline to be aware of. To open a Trump Account and claim the $1,000 seed deposit, file IRS Form 4547 with your 2025 tax return or register online at trumpaccounts.gov. The IRS will begin sending account activation information in May 2026, with accounts going live on July 5, 2026.

If you have a child or grandchild born between 2025 and 2028, this is one of those rare moments where doing something small now could have an enormous impact on their financial future. Children born before 2025 will not receive the $1,000 government contribution, but parents can still open accounts for children under 18 and contribute up to $2,500 pre-tax annually on their behalf.

Why This Matters for the Next Generation of Homebuyers

We talk a lot about affordability challenges in the housing market today, and those challenges are real. But the buyers who will feel today’s conditions most acutely are the young people who are still years away from purchasing their first home. Giving them a head start right now, no matter how small it seems today, is one of the most meaningful things we can do for their financial future.

Financial advisors have been saying for decades that early investing is the single most powerful wealth-building tool available to everyday families. A Trump Account is one concrete way to put that principle into action for the children in your life.

Let’s Talk About Building a Future for Your Family

Whether you are thinking about buying a home now or planning ahead for the next generation, I am here to help you think through the big picture. If you have questions about how to set your family up for long-term financial success through homeownership, reach out today. Let’s have that conversation.

You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

Subscribe and Read More

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!