If you have ever wondered why so many financial advisors, parents, and grandparents push homeownership so hard, it is not just tradition talking. There is real math behind it. And once you understand how the wealth gap between homeowners and renters actually works — not just that it exists, but how it compounds over time — it becomes one of the most compelling arguments for buying a home that you will ever hear.

The good news is that for buyers in New Jersey who feel priced out, there are programs specifically designed to help bridge that gap. But first, let us break down the mechanics.

The numbers here are striking enough that they deserve to be stated plainly before anything else.

In 2025, the net worth of the typical homeowner sits at around $430,000, compared to roughly $10,000 for the average renter — a 43-to-1 difference, according to an analysis of Federal Reserve data by the National Association of Realtors.

That is not a typo. A homeowner’s net worth is 43 times greater than a renter’s. And what makes this number even more sobering is the direction it is heading. Comparing 2019 to today, renters have grown their wealth by 37%, while homeowners got about 46% wealthier. As the net worths of both groups have grown, so has the wealth gap between them.

Even setting aside home equity entirely, the difference remains enormous. Even when excluding home equity, homeowners still maintain 606% more wealth than renters. That tells you that homeownership does not just build wealth through property value — it fundamentally changes how people save, invest, and accumulate assets across their entire financial life.

Most people understand the concept that a home builds equity. But the mechanism behind it is worth slowing down on, because it is more powerful than most renters realize.

Homeownership builds wealth by pulling three levers at once: monthly mortgage payments gradually increase owners’ equity, rising home values contribute to that equity, and the earlier a buyer gets in, the longer those gains can compound. That helps explain why homeowners’ net worth so dramatically outpaces renters’ — and why delayed or denied access to homeownership can have lasting consequences across generations.

Think about what happens every month when a renter pays rent versus when a homeowner makes a mortgage payment. Both are paying for a place to live. But the homeowner’s payment is doing double duty. With a mortgage, part of that payment eventually ends up back in your pocket. Renters, on the other hand, do not have access to that same mechanism — they also make a monthly housing payment, but it does not build equity or create an ownership stake that can later be sold, borrowed against, or passed down.

Meanwhile, the cost of renting keeps going up. 53% of renters, roughly 24.7 million households, spend more than 30% of their household income on rent, while 28% spend over 50% of their income on housing costs. Homeowners, by comparison, spend an average of just 16.4% of their income on housing. Every dollar a renter spends above and beyond what a homeowner would pay is a dollar that never comes back.

One of the most important things to understand about building generational wealth through homeownership is that the earlier you get in, the more dramatically the outcome changes.

The earlier someone buys, the bigger the payoff can be. A household that purchases at a younger age has more years to build equity through principal paydown and more years to benefit from rising home values. While most Baby Boomers owned their home by age 30 — the critical age to maximize the long-term benefit — only 42% of Millennials owned their home at the same age.

First-time homebuyer activity is at historic lows, with only 21% of home purchases in 2025 made by first-time buyers, down from 34% in 2021. High prices, high mortgage rates, and large down payment requirements are delaying ownership for many younger households. Every year that delay continues is a year of compounding equity that a buyer never gets back.

The typical renter now pegs their chances of ever owning a home at just 33.9%, the lowest reading on record in a decade-long tracking survey by the New York Federal Reserve. And a 2023 Federal Reserve Bank of Philadelphia study found that rising rents push renters further into debt and delinquency, as more of their earnings go toward basic living expenses. It is a cycle that feeds itself — and one that the right programs can help break.

Both state and federal governments understand that the wealth gap created by limited access to homeownership has long-term consequences — not just for individual families, but for entire communities. That is why targeted programs exist specifically to help first-time and lower-income buyers get a foot in the door.

The federal government can reduce rental cost burdens and expand homeownership opportunities by providing targeted down payment assistance for first-generation homebuyers who lack generational wealth, along with expanding housing choice vouchers to help renters build savings for down payments.

Here in New Jersey, the support available goes well beyond what most buyers realize when they first start looking.

New Jersey is one of the most expensive housing markets in the country, but it also offers some of the most generous assistance programs available anywhere in the nation — and most first-time buyers have no idea they exist.

The New Jersey Housing and Mortgage Finance Agency’s First-Time Homebuyer Mortgage Program provides qualified buyers with a competitive 30-year, fixed-rate government-insured loan originated through an NJHMFA participating lender. That loan can be paired with significant financial assistance on top of it.

Under the NJHMFA Down Payment Assistance Program, qualified borrowers can receive up to $10,000 in assistance funds toward closing costs or a down payment, structured as a zero-interest, five-year forgivable second mortgage with no monthly payments. As long as the borrower lives in the home for five years, the loan is forgiven completely.

For buyers who are the first in their family to own a home, the assistance goes even further. First-generation buyers — those who have never owned a home and whose parents did not own one — may receive an additional $7,000 in assistance on top of the standard program, bringing combined forgivable assistance to $22,000. Both the standard assistance and first-generation support are forgivable after five years of continuous occupancy.

And for buyers who qualify at or below 80% of area median income, there is an additional layer available. The Homebuyer Dream Program, funded through the Federal Home Loan Bank of New York, allocated $31.67 million in 2026 and offers grants of up to $30,000 per household toward down payment, closing costs, and homebuyer counseling services, through participating member banks across New Jersey and New York.

When these programs are stacked together strategically, the results can be significant. In some cases, buyers who qualify for multiple programs combined can receive up to $52,000 toward their purchase when NJHMFA programs and nonprofit New Jersey Community Capital assistance are layered together.

Generational wealth is not a concept reserved for people who are already wealthy. It is built one purchase at a time, one mortgage payment at a time, over years and decades. The families who are passing something meaningful on to their children are very often the families who bought a home when buying felt hard, not easy.

With a fixed-rate mortgage, the bulk of your cost is locked in. Renters face unpredictable rent increases and have less control over their housing expenses, making long-term planning harder. Even during slow market years, your home remains tied to a real asset that is growing your net worth. That stability alone is worth more than most renters account for when they compare the cost of renting versus buying.

The programs are there. The opportunity is real. And the longer someone waits, the more of that compounding growth stays out of reach.

If you have been renting and wondering whether homeownership is something you can actually reach right now, let’s have that conversation. I work with lenders who know these programs inside and out and can help identify exactly what assistance you may qualify for. The path to building your own generational wealth might be closer than you think. Reach out today and let’s take a look at your options together.

You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

Not too long ago, the checklist for buying a home was pretty straightforward. Price, location, school district, commute. Maybe a quick look at the neighborhood. But the conversation has shifted in a real and undeniable way, and buyers here in New Jersey are asking questions during home searches that simply were not on anyone’s radar a decade ago.

Climate risk is now part of the purchase decision, and honestly, it should be.

If you need a vivid, real-world example of what climate risk looks like when it reaches its worst possible outcome, look no further than Rancho Palos Verdes in California. This is not a hypothetical or a distant scenario. This is a wealthy coastal community where the ground beneath homes has been literally moving, and no amount of money has been able to stop it.

NASA and city monitoring revealed that land in the Portuguese Bend area was sliding at a rate of 5 to 9 inches per week — far faster than the inches-per-year rate seen previously. Heavy rains in 2023 and 2024 reactivated dormant slide areas, accelerating ground movement. Homes collapsed, fissures cracked roads, buckled walls, and damaged utilities.

As recently as February 2026, the Abalone Cove Landslide accelerated by an average of five percent to approximately 2.24 inches per week, while the Portuguese Bend landslide accelerated by about 7.1% to roughly one and a half inches per week, with the city believing that recent rainfall was the most likely contributing factor.

The city’s landslide response is expected to cost $64.4 million by the end of June 2026, and Rancho Palos Verdes has applied for a $48.7 million FEMA Hazard Mitigation Grant for the Portuguese Bend Landslide Remediation Project. Even with all of that money and effort, the land keeps moving. Homeownership should never come with that kind of uncertainty underneath it.

What is happening in California is an extreme case, but the broader data tells us that climate vulnerability in the housing market is not just a coastal California problem.

More than one in four U.S. homes, amounting to $12.7 trillion in real estate, faces at least one type of severe or extreme climate risk, including floods, hurricanes, and wildfires, according to a Realtor.com Climate Risk Report. Nearly 6 million homes valued at $3.4 trillion face severe flooding risk over the next 30 years, roughly 2 million more than FEMA currently estimates, because federal flood maps do not account for heavy rainfall and future climate changes.

Flooding, fire, drought, and other weather-related risks have always been a danger to property and consumer wellbeing. However, with the changing climate, these risks are increasing in intensity and frequency, impacting the likelihood of damage, the cost of utilities, the price of insurance, and the potential resale value of homes.

The insurance picture is equally sobering. Insurance premiums are surging in high-risk markets, with Miami homeowners paying an average of 3.7% of a home’s value in annual premiums — the nation’s highest rate. The sharp rise in premiums, increased frequency of disaster events, and growing difficulty in securing coverage are reshaping not only where people live but also whether housing remains affordable in vulnerable regions.

This is not just someone else’s problem. Here in New Jersey, climate risk is a very real and growing part of the housing conversation.

Sea levels along the Jersey Shore have risen about a foot and a half since the early 1900s, more than twice the global average according to Rutgers University, as climate change drives ocean levels higher and the land itself sinks. In places like coastal New Jersey, sea levels are rising and the land is sinking, and experts say the safest option is to move people out of the riskiest flood zones, though that is not always practical.

Research from Rutgers University found that New Jersey can expect to see roughly five feet of sea level rise by the end of the century under a moderate-emissions scenario, and an estimated 62,000 homes along New Jersey’s coast will experience chronic flooding by 2050, leaving tens of thousands of homeowners facing skyrocketing flood insurance rates, loss of property value, and eventual displacement.

New Jersey has responded with new policy. The state unveiled new tools and technologies designed to provide prospective homebuyers and renters with critical information needed to make better informed decisions on where they choose to live and how best to protect their property from flood damage, with flood disclosure requirements described as some of the strongest in the nation.

The shift in buyer behavior is measurable and well documented. It is not just cautious buyers making different choices — even investors and buyers with a high tolerance for risk are stepping back from properties flagged for climate vulnerability.

When told about risks from flooding, prospective homebuyers were significantly less likely to make offers on vulnerable properties, according to research from Redfin involving more than 17 million prospective buyers. Redfin’s chief economist noted that as more buyers become aware of climate risk, homes in endangered areas will likely receive fewer offers, causing home values to fall.

A 2025 study shows that 50% of Gen Z and 56% of Millennials prioritize climate risks when deciding where to live, compared to 31% of Boomers and 40% of Gen X. The next generation of buyers is not going to ignore this the way previous generations may have.

As insurance becomes harder to secure in risk-prone areas, markets in lower-risk regions are expected to see stronger home price growth due to climate-driven migration. Where people choose not to buy matters just as much as where they do.

The good news is that information is available if you know where to look, and asking the right questions before you make an offer costs you nothing.

Start with flood history. Past flood damage can be hidden, costly to repair, and a sign of future risk. Some major real estate websites already include flood risk and other climate risks in their listings, and it is important to check whether your state has disclosure requirements for past flooding.New Jersey now has strong disclosure laws, which means sellers are required to be transparent about flood risk in ways they were not before.

Think about insurance before you fall in love with a property. A professor of real estate at the University of Pennsylvania’s Wharton School advises prospective buyers to consider whether they can still afford the property if insurance premiums double or triple. That is a question worth sitting with before you sign anything.

And remember that being outside a FEMA flood zone does not mean you are safe from flooding. On average, 40% of National Flood Insurance Program flood insurance claims occur outside of high-risk flood areas. The maps are outdated in many places, and the weather is no longer behaving the way those maps were drawn to reflect.

This is one of the most important reasons to work with a licensed real estate professional rather than navigating a home search on your own through public websites. When you browse listings on Zillow or similar platforms, you are seeing a curated, surface-level view of a property. As your realtor, I have access to a much deeper layer of information that simply does not appear on those sites.

That includes seller disclosures, which require sellers to reveal known issues with the property, including past flooding, water intrusion, and structural concerns. I can pull FEMA flood maps and cross-reference them against the actual property boundaries, not just the general area. I have access to flood zone certifications, historical MLS data that may show prior price reductions tied to climate-related issues, and community-level information about drainage, municipal infrastructure, and known problematic streets or neighborhoods. I can also connect you directly with insurance professionals early in the process, before you fall in love with a house, so you know exactly what coverage will cost before you commit.

The difference between what is publicly available and what I can access on your behalf is significant. That information could easily be the difference between a sound investment and a costly mistake.

None of this means you should stop looking for a home. It means you should look with better information. The buyers who are winning right now are the ones who understand what they are buying into, not just the price and the square footage, but the full picture of long-term risk and long-term value.

Climate risk is not a reason to sit out the market. It is a reason to have a more informed conversation about which properties make sense for your future.

If you are searching for a home in New Jersey and you want someone in your corner who will help you ask the right questions and look at the full picture — including what the property looks like 10 and 20 years from now — let’s talk. Reach out today and let’s start that conversation.

You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

If you have been feeling like homeownership seems further out of reach than it used to be, you are not imagining it. New data from the National Association of Home Builders puts real numbers behind what so many buyers are already feeling, and the picture it paints is worth understanding before you decide your next move.

NAHB recently released its 2026 Priced-Out Analysis, and one of the most powerful tools within it is what they call the housing affordability pyramid. Think of it as a visual breakdown of exactly how many American households can actually afford to buy at each price point.

The pyramid reveals that 52% of households, roughly 70 million, cannot afford a $300,000 home, while the estimated median price of a new home sits around $410,000 in 2026. Read that again. More than half of all households in this country cannot afford a home that costs less than the median new home price. That gap is not a small one, and it matters deeply for buyers who are trying to figure out where they actually stand.

The pyramid is built around income thresholds and standard underwriting guidelines, which makes it a practical tool rather than just a theoretical one.

The minimum income required to purchase a $200,000 home at a mortgage rate of 6% is $55,500. In 2026, about 47.5 million households in the U.S. are estimated to have incomes at or below that threshold, meaning they can only afford to buy homes priced up to $200,000. These 47.5 million households form the bottom step of the pyramid. Of the remaining households that can afford a home priced at $200,000, an additional 22.4 million can only afford to pay somewhere between $200,000 and $300,000. Each step above that narrows further as prices rise.

What makes this even more telling is the supply side of the equation. While around 47.5 million households can only afford a home priced at $200,000 or less, there are only 20.7 million owner-occupied homes valued in that price range. That same imbalance continues in the $200,000 to $300,000 range, where the number of households that can afford homes far exceeds the number of homes actually available. The Mortgage Reports It is not just an income problem. It is a supply problem layered on top of it. (Eye on Housing / NAHB)

Here is where I want to shift the conversation, because data like this can feel discouraging if you stop there. The pyramid shows us the challenge clearly, but it does not show us the full picture of what is actually available to buyers who know where to look.

Special home financing programs exist specifically for this moment. They are designed to help low-income and first-time buyers bridge the gap between where they are financially and what the market requires, and more people qualify for them than realize it. The most widely used programs include FHA loans requiring just 3.5% down, USDA loans and VA loans that offer 0% down payment options, and conventional programs like HomeReady and Home Possible that require only 3% down

Beyond loan types, there is meaningful grant money available that does not need to be paid back. Grants of up to $25,000 typically do not require repayment if residency requirements are met, and many programs are designed for specific groups such as teachers, healthcare workers, or low-income buyers.

Down payment and closing cost assistance is available in a variety of forms across cities and counties throughout the United States, including grants, zero-interest loans, and deferred payment loans. Most buyers simply do not know these programs exist until someone walks them through them.

If you are not sure where to start, there are government-backed options that cover a wide range of situations. FHA loans offer assistance to first-time homebuyers and carry a lower credit score requirement than most conventional home loans. USDA single-family housing programs are available to buyers in rural areas, and the VA Home Loan program helps veterans, surviving spouses, and active-duty service members purchase homes with favorable terms.

State-level programs can be equally powerful. In New Jersey, for example, first-time buyers can receive up to $15,000 in down payment assistance through a five-year forgivable loan with no interest and no monthly payments required, and first-generation buyers may qualify for an additional $7,000 in assistance. Programs like this exist in nearly every state, and the specifics vary significantly by location.

Even some banks have stepped up with direct assistance programs. Bank of America’s Down Payment Grant program offers a grant of up to 3% of the home purchase price, up to $10,000, which does not require repayment, and their America’s Home Grant program offers an additional lender credit of up to $7,500 toward closing costs.

The numbers in this year’s affordability analysis are real, and the challenges for buyers at lower income levels are real too. But challenges are not the same as impossibilities, and knowing the right programs, the right lenders, and the right strategies makes an enormous difference in what becomes possible for you.

We work with mortgage lenders who know these special financing programs inside and out. They understand how to match buyers to options that fit their specific situation, and they have helped people find pathways to homeownership that those buyers never thought were available to them.

If you are wondering whether homeownership is within reach given where you are financially right now, let’s have that conversation. I can connect you with the right lenders, walk you through what programs may apply to your situation, and help you understand exactly where you stand. Reach out today and let’s start with a real conversation about what your path to homeownership actually looks like.

You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

Buying or selling a home is one of the biggest financial decisions of your life. And right now, there are people out there using some of the most sophisticated technology ever created to steal from you during that process. I want to talk about something that I think every single person in a real estate transaction needs to understand before they wire a single dollar or sign a single document.

Deepfakes are no longer a science fiction concept. They are here, they are convincing, and they are being used specifically to target real estate transactions.

A deepfake is an AI-generated video, image, or audio recording that mimics a real person’s face, voice, and mannerisms so accurately that even sharp, attentive people can be fooled. With as little as 30 seconds of audio, fraudsters can replicate someone’s voice with unsettling precision. What once demanded Hollywood-level expertise can now be done in mere hours for under $10 a month. That is not a typo. For less than the cost of a streaming subscription, a criminal can become you, your agent, your attorney, or your title officer.

Deepfake scams have increased 40% year-over-year, according to the 2026 Identity Fraud Report by security firm Entrust. This is not a fringe threat. It is a rapidly growing one that is hitting real estate especially hard because of the large sums of money involved and the high level of trust required between all parties in a transaction.

Here is why scammers love real estate: the transactions are enormous, they involve multiple parties, and a lot of the process has moved online. As the homebuying process has shifted increasingly to digital documents and remote communication, it has also created new opportunities for fraud. Scammers are not randomly picking victims. They are strategically targeting an industry where six-figure wire transfers happen every single day.

In one documented incident, scammers created a deepfake video of a property owner authorizing a wire transfer, tricking both a buyer and an agent and resulting in hundreds of thousands of dollars in losses. In another case, a Florida title company scheduled a video call to confirm the identity of a seller on a vacant lot, only to discover they were communicating with an entirely AI-generated person. The technology had become so refined that the fraud was only caught because the title company was specifically looking for it.

A British engineering firm sent $25 million to scammers after AI-generated deepfakes convinced a finance worker that the people on a video call were real. If a sophisticated international company can be deceived in a board-level video call, buyers and sellers in the middle of an already emotional and stressful transaction are absolutely at risk.

Deepfakes and wire fraud go hand in hand, and this is where real estate transactions become most vulnerable. Cybercriminals hack or spoof legitimate email addresses belonging to real estate agents, title companies, or attorneys. Once inside the communication thread, they quietly monitor the transaction and wait for the right moment to send convincing messages with “updated” wire transfer instructions that redirect funds to a fraudulent account. Once sent, that money often disappears within hours through a web of international accounts.

Real estate fraud cost Americans $16.6 billion in 2024, with wire fraud being the fastest-growing threat to home buyers. The median financial loss for wire fraud victims in real estate exceeds $70,000 per incident. And here is the part that should stop everyone cold: once that wire goes out, it is nearly impossible to recover.

Not every deepfake is perfect, and knowing what to look for gives you a real advantage. Watch for unnatural lighting with shadows or brightness that looks off, blurry or distorted faces, mismatched skin tones, eyes that blink too much or too little, awkward head movements, robotic-sounding voices, or background noise that does not quite fit the scene. These subtle inconsistencies are the tells that the technology has not yet learned to fully eliminate.

That said, the technology is improving fast. Which is why the most reliable protection is not digital at all.

This is the most important thing I can tell you: meet in person before you make any financial transaction. I know that feels old-fashioned in a world where we do everything remotely. But no deepfake can shake your hand. Always verify the identity of the person you are dealing with through multiple sources and whenever possible, meet in person to confirm details before proceeding.

Always verify wiring instructions by talking directly to the receiving party by phone on a known number, or meeting in person. Never rely solely on digital copies of property documents that could have been altered. If someone you are working with in a transaction resists meeting in person or insists on communicating only through digital channels, that is a red flag worth pausing on.

Nearly one in four consumers received suspicious communications during their closing, and of those targeted, one in 20 became victims. A quick in-person verification is a small inconvenience compared to losing your down payment.

Beyond meeting face to face, there are concrete things you can do right now to protect yourself and your transaction.

Ask your title company about multifactor authentication before transferring funds or signing important documents. Many companies are now using third-party verification tools. Consider investing in an owner’s title insurance policy to safeguard against forged deeds, fraudulent liens, and fake ownership claims.

If you receive updated wiring instructions at any point, do not act on them until you have called your title company directly using a phone number you already have on file, not a number included in the suspicious message. This one step has stopped countless frauds in their tracks.

And if something feels wrong, trust that feeling. The urgency scammers create is intentional. They want you to move fast before your instincts catch up with you.

This is exactly why the relationship you have with your real estate agent matters so much. When you work with someone you have met, spoken with, and built trust with over time, it becomes much harder for a scammer to insert themselves into the process undetected. You already know what your agent sounds like, what they look like, and how they communicate.

Deepfake technology is convincing precisely because it targets strangers. The more familiar you are with the real people in your transaction, the better protected you are.

If you are thinking about buying or selling and you want to make sure every step of your transaction is handled safely and with full transparency, let’s connect. I work hard to keep my clients informed, protected, and never caught off guard — especially when the stakes are this high. Reach out today and let’s talk through what a safe, smart transaction looks like for you.

You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

The Original Pancake House in West Caldwell

West Caldwell‘s story doesn’t start with a strip mall or a highway interchange. It starts with a minister who rode over mountains to preach to people who needed him. James Caldwell, the man after whom the Caldwells are named, earned the nickname “the Fighting Parson” during the Revolution for his service alongside Washington’s men in Horseneck. When the war ended, the community honored him by renaming their home “Caldwell” in 1798. That kind of history is baked into this town’s identity, and it still shows today in the way neighbors show up for each other.

The area that would become West Caldwell was originally known as Westville, owned predominantly by the Crane and Harrison families, and was home to farming lands and a local sawmill. Not glamorous, perhaps, but deeply practical and community-driven in a way that still echoes in how the town operates today.

By 1904, growth across Caldwell Township had made it difficult for residents on opposite ends of town to agree on public improvements. So on February 16, 1904, West Caldwell was incorporated as its own borough — covering 3,175 acres and home to 410 people. That quiet act of self-determination set the tone.

Over a century later, the town is now recognized as one of the most beautiful residential communities in all of Essex County. That reputation didn’t come from marketing. It came from people who cared enough to build something worth staying in.

If you’ve driven through West Caldwell even once, you’ve probably already gotten a sense of it. Bloomfield Ave and Passaic Ave cut right through the center of town, and that’s where most of the action is — restaurants, shops, and that low-key energy of a town that knows what it is. You’re also minutes from Route 46 and Route 280, which makes the daily commute or a weekend trip to the city surprisingly painless.

What you might not immediately notice is that West Caldwell has a real working commercial backbone. There are companies and warehouses operating here, but they’re tucked behind the scenes, out of sight and out of mind for most residents. The residential streets feel exactly as calm as they look, which is rare when a town sits this close to major transit corridors.

And then there’s the Mountain Ridge Country Club. Yes, there is a beautiful mountain ridge country club right here in West Caldwell. It’s the kind of amenity that surprises people who assume it’s only found in more expensive neighboring towns.

The schools are another draw worth knowing about. West Caldwell’s school system consistently ranks well, and families tend to appreciate the academic focus. A few parents do wish there were more AP course offerings at the high school level, so if that’s a major priority for your household, it’s worth a closer look. But overall, the educational environment here is solid, and it’s one of the more frequent reasons families choose to put down roots.

It’s a town that feels genuinely settled. Well-kept homes, tree-lined streets, green spaces where kids actually play, and local events that bring people out of their houses and into each other’s company. Whether you’re a young family looking for stability, or a professional who wants quiet evenings and quick highway access, West Caldwell has a way of fitting the bill.

If there’s one place in West Caldwell that functions as an unofficial community gathering spot, it’s Sam’s. On weekends especially, you’ll see high schoolers and longtime residents lined up side by side, which tells you everything you need to know about the kind of shop this place is. People drive in from surrounding towns just to get their bagel fix here, and honestly, you understand why the moment you hold one in your hand.

My personal go-to is about as simple as it gets: an everything bagel with scallion cream cheese. No frills, no fuss, just perfect. But the sandwiches are genuinely to die for. Whatever you’re in the mood for, they’ve got a combination that’ll become your regular order within about two visits.

This place has been feeding West Caldwell residents since 1968, and it has earned every single one of those years. On holidays and weekends, even on regular weekdays, the place is packed. Their menu dedicates an entire page just to pancakes, which should give you a sense of how seriously they take the craft.

If you lean sweet, the Georgia Pecan Pancakes are the move: the ratio of pecans to pancake batter is genuinely perfect. If you’re a savory breakfast person, the corned beef hash is great, and their combos run the range from farm fresh sausage links all the way to steak and eggs. They also offer gluten-friendly pancake options, which is a thoughtful touch for a place that’s been around this long.

The Original Pancake House isn’t trendy. It’s just consistently excellent, and that’s a harder thing to pull off than most people realize.

Franco’s has been part of this community since 1976, and under the current father-and-son ownership (a duo from Ischia, Italy who took over in 2013), it’s only gotten better. The pizza is delicious and the pricing is genuinely fair, which in North Jersey is not something you take for granted. But the dinner menu is where Franco’s really shines: the portion sizes are enormous and the quality matches every bite.

Personal favorites? The Veal Parmigiana, Chicken Marsala, Baked Ziti Bolognese, and the Penne Vodka pizza — yes, a penne vodka pizza, and yes, it absolutely works. They also run weekly specials and family deals that make a solid sit-down dinner feel like a steal. The kind of place you bring out-of-town guests and watch them immediately ask for the address to take home.

PF started as a family-run retail fish market back in 1978, and the sit-down restaurant side opened around 2010. So the seafood credibility here runs deep, quite literally. What sets this place apart is that they operate an on-site fish market, which means the freshness is not a marketing claim, it’s a fact. You’re eating what came in today.

It’s a bit more expensive than the other spots on this list, and it’s worth knowing they’re closed on Mondays. Their raw bar comes highly rated by people who know their seafood and is consistently one of the first things regulars recommend. If fresh, quality seafood is your thing, PF is the obvious answer in West Caldwell.

Here’s the real deal: West Caldwell doesn’t currently have a dedicated coffeeshop. If you’re the type who needs a local café to settle into with your laptop or meet a friend over a latte, you’ll want to make a short trip to neighboring towns like Caldwell or Montclair, which have plenty of great options.

It’s a genuine gap in the local scene — and honestly, it might be an opportunity waiting to happen. For now, the bagel shops fill some of that morning ritual need, and they fill it well.

If you haven’t been in yet, put it on your list. The new ShopRite opened in October 2025 at 900 Bloomfield Avenue, and it’s a genuine upgrade for the community. We’re talking nearly 90,000 square feet, which is almost twice the size of the old location. It includes a food court seating area right in the middle of the store, expanded fresh departments, and a full wine, beer, and spirits section with three aisles of curated selections.

The old Passaic Avenue location, which opened in 1967, was beloved for its distinctive red pagoda roofline — a design inspired by founder Irving Gladstein’s deep appreciation for Japanese architecture and culture, rooted in his World War II service in the Pacific theater. To honor that history, archival family photos are on display at the new location, and iconic elements like the Asian-inspired phone booths made the move too.

Today, Dara Sblendorio, the fourth generation of the founding Gladstein family, leads Sunrise ShopRite as its president. The grand opening included a full community parade from the old store to the new one on Bloomfield Ave, which is not a chain store thing. That’s a family business saying thank you to the town that kept them going for generations. The new store is modern, massive, and easy to navigate. If grocery shopping is your primary errand, this one genuinely makes the list of reasons to love living here.

If you are thinking about buying or selling in West Caldwell, you are not just choosing a house. You are choosing a true suburban town that has strong schools and a town that keeps quietly improving. If you want to talk about which pockets of town best fit your lifestyle, commute, and budget, please reach out. We can walk through the neighborhoods together so you can feel the vibe for yourself before you make a move.

If you have any real estate needs, I’m the realtor for you! You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

Property taxes are one of the biggest ongoing costs of owning a home in New Jersey, and they are also one of the least understood. New Jersey has the highest average property tax bills in the nation, now topping ten thousand dollars a year on average, so it is no surprise that homeowners feel stressed and want clarity.

That is exactly why the New Jersey Society of CPAs, New Jersey Realtors and the Association of Municipal Assessors created a full guide just to help you understand what you are paying for and why.

One reason property taxes feel so confusing is that each municipality has its own assessed values, budgets and tax rates. A Certified Municipal Assessor in your town is responsible for setting the value of every property, usually based on market value and updated through reassessments, appeals or major changes like renovations and new construction.

This means two homes that look similar in different towns can carry very different tax bills because their assessments and local tax rates are not the same.

Your tax bill is not a random number, even if it sometimes feels that way. Each year, your town, your county and your local school system put together budgets that subtract out other revenues like state aid, grants and fees, and whatever is left becomes the “tax levy” that must be raised from property owners.

The County Board of Taxation then sets a tax rate using the total assessed value, called ratables, and your municipal tax collector applies that rate to your specific assessment to calculate your bill.

It helps to remember that your property tax payment is really supporting several layers of local services, not just “the town.” On average across New Jersey, about fifty two percent of the total tax levy goes to schools, thirty percent goes to the municipality, and eighteen percent goes to the county. Those dollars help fund K–12 education, police and fire protection, parks, roads, and other public services that you and your neighbors rely on every day.

Behind the scenes, there is a predictable calendar that repeats every year, even if you only notice the four due dates on your bill. Assessors begin setting values in October for the next year, budgets are developed and adopted in the first half of the year, and the County Board of Taxation sets the final tax rates before bills go out.

You then see that work show up as quarterly payments due in February, May, August and November, with the first two quarters often based on estimates from the prior year and the last two used to “true up” to the final annual amount.

Because your assessment is one half of the tax equation, it is important to know how and why it was set. Residential properties are meant to be assessed at market value, but in practice values can lag the market unless your town does regular revaluations or uses an approved annual reassessment program.

If you believe your assessment is higher than what similar homes in your area would sell for, New Jersey law gives you the right to appeal each year within a specific window using the information on your Notice of Assessment.

Once you or your mortgage company pay the bill, the story does not end there. Your town is responsible for splitting and sending those funds to the school district, county and any special taxing districts such as a fire district, library or open space fund. The distribution is done according to the budgets and levies that were set earlier in the year, so every timely payment helps keep those essential services funded and running smoothly.

Because local governments rely heavily on property taxes to operate, late payments come with serious consequences in New Jersey. Most towns charge interest on overdue taxes back to the original due date, often at rates allowed by state law that rise as delinquencies grow.

If taxes remain unpaid through the fourth quarter, a tax lien can be placed on the property and eventually sold at public auction, and if it is not redeemed within the legal time frame the owner can even lose the property and any equity.

Property taxes will probably never be anyone’s favorite bill, but understanding how they are calculated and where they go can make them feel less mysterious and less random. The New Jersey Homeowner’s Guide to Property Taxes was created so you can see the full path from assessment to budget to rate to bill to disbursement, and ask better questions of your town, your tax professionals and your real estate agent.

When you know how the system works, you are in a stronger position to plan your budget, evaluate different towns and protect your investment as a homeowner.

If property taxes are a big part of your housing decisions or you are comparing towns and school districts, let’s sit down and walk through your current bill and what it would look like in a new home. I can help you interpret the numbers, connect you with tax and mortgage professionals when needed, and factor real property tax costs into your buying or selling strategy so there are fewer surprises and more confidence in your next move.

If you have any real estate needs, I’m the realtor for you! You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

Now is a great time for many sellers, especially with 2026 still expected to slightly favor homeowners who choose to list. At the same time, it is completely normal to feel hesitant, especially if you have lived in your home for many years and it holds a lot of memories. However, there is no one “perfect” time to sell for everyone, only the right time for you once you understand your reasons.

Maybe your household has grown, maybe it has shrunk, or maybe your daily routines and hobbies look very different than when you first moved in. If your home now feels too small, too big, or simply not set up for your current season of life, that is a valid reason to start thinking about selling and finding a better fit.

Life circumstances like a new job, a longer commute, changes in your health, or the needs of aging family members can suddenly make your current location less practical. Career or lifestyle shifts are some of the most common reasons people decide it is time to move, even if they still love their house itself. If your home is making everyday life harder instead of easier, that is an important signal to pay attention to.

For many families, children change everything from school priorities to space needs to access to parks and activities. You can love your neighborhood and still realize it is no longer the best setup for your kids, whether that means wanting a different school zone, more bedrooms, or a safer and quieter street. I want to remind you that your home should support your family’s well‑being, not squeeze you or your children into a lifestyle that no longer works.

Maybe your children have moved out and you are now maintaining more space than you use, or the stairs and yard work feel heavier than they did a decade ago. Many longtime owners reach a point where the upkeep, repairs, and carrying costs simply no longer match their energy or priorities. Downsizing or moving to a more turnkey home can free up both equity and mental space, which is a powerful reason to at least explore your options.

There is the personal side, and then there is the market side. Economists expect 2026 to bring more inventory, slightly lower or steady mortgage rates, and modest price growth, which together point to a healthier but still seller‑leaning market in many areas. A high‑demand market can be an advantage for sellers, but your agent should still help you look closely at local data, not just national headlines.

Interest rates are a big reason many owners have stayed put, especially if you locked in a lower rate a few years ago. At the same time, strong price growth over the last decade means a lot of homeowners are sitting on significant equity that could be used for a move, a downsize, or even a lifestyle change. It might not be the right time to sell if you lack enough equity or are committed to keeping a very low rate, but if you do have equity and your life has shifted, it is worth running the numbers instead of assuming a move is out of reach.

Some sellers are simply tired. Constant projects, rising repair costs, and never‑ending to‑do lists can make what once felt like a dream home start to feel like a burden. NAR’s guide talks about the idea of being “ready for a turnkey home,” one that is easier to maintain so you can focus more on living and less on fixing. If your home is creating more stress than joy, listening to that feeling is just as important as watching interest rates.

When you stack all these factors together, a simple pattern shows up. The right time to sell is less about predicting the absolute top of the market and more about whether your home still fits your life, your finances, and your future plans. I encourage you to answer these questions honestly and then sit down with a trusted real estate professional to talk through timing, preparation, and pricing, instead of making a rushed decision or staying frozen in uncertainty.

If you are wondering whether now is truly the right time for you to sell, let’s talk through these seven factors together in the context of your own life, not just the market headlines. I will walk you through your options, your equity, and our local trends so you can make a clear and confident decision about staying, selling, downsizing, or moving on to your next chapter.

If you have any real estate needs, I’m the realtor for you! You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

If you have ever sat down with a financial advisor, chances are they talked your ear off about compound interest. And they were right to. The earlier money starts growing, the more dramatically it multiplies over time. That principle is at the heart of a new federal program that every parent, grandparent, aunt, and uncle should know about right now, regardless of where you fall politically.

This is not about politics. This is about a real financial opportunity for the children in your life.

Trump Accounts are a new type of individual retirement account created for eligible children, established under the Working Families Tax Cuts Act. Parents or guardians can open and manage the account on behalf of their child, and the federal government will make a one-time $1,000 pilot contribution to the account of each eligible child who is a U.S. citizen born on or after January 1, 2025, through December 31, 2028.

Think of it as a baby shower gift from the federal government, except instead of a onesie, it is a financial foundation. This gift is not meant to be unwrapped until your child turns 18, giving the investment time to compound and eventually be put toward life’s biggest milestones, like going to college or buying a house.

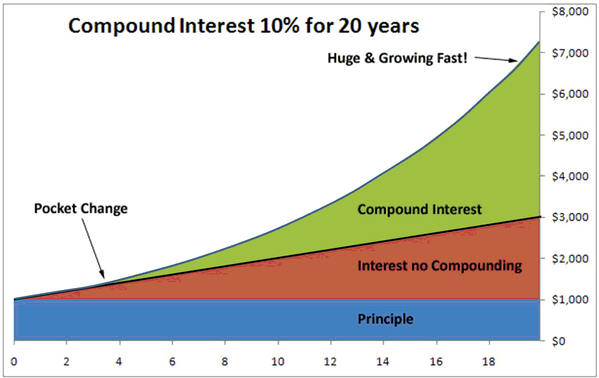

This is where compound interest does its quiet, powerful work, and the numbers are worth sitting with for a moment.

For an account created at birth with the $1,000 seed investment and no other contributions, the Treasury estimates the account could grow to about $6,000 at 18 years old, $15,000 at 27, and $243,000 at 55, assuming an average annual return of about 10.5%.

Now imagine what happens if a family adds to that account along the way. If a family contributes and invests the full $5,000 annually for all 18 years, assuming a 6% annual growth rate, the account could hold around $191,000 in assets by the time the child turns 18. Even if no additional contributions are made after that, by the time the beneficiary reaches age 60, the account could be worth more than $2.2 million.

That is the power of starting early. Every year of growth matters, which is exactly why this program is worth paying attention to now rather than later.

Here is the part that connects directly to homeownership. When your child turns 18, they can use the funds for specific purposes, including paying tuition, starting a business, or making a down payment on a home.

Given how challenging the path to homeownership has become for younger generations, having an account earmarked and growing from birth is a meaningful advantage. The down payment hurdle is one of the biggest barriers first-time buyers face. A Trump Account does not solve that problem overnight, but 18 years of compound growth can make a real dent in it.

The $1,000 from the federal government is the floor, not the ceiling. Families can contribute up to $5,000 per year, and employers can add another $2,500 pre-tax through employer cafeteria plans, effectively creating a new pre-tax savings vehicle for families. Charitable organizations and government entities can also make contributions that do not count against the $5,000 family limit.

Several major companies have already pledged to match employee contributions to Trump Accounts, including JPMorgan Chase, IBM, and Comcast. And Michael Dell and his wife Susan Dell announced a $6.25 billion donation to fund accounts for 25 million children, contributing $250 per account for children under 10 in lower-income zip codes.

The investments inside the account are intentionally simple. Funds must be invested in low-cost index mutual funds or ETFs focused primarily on U.S. companies, with an expense ratio cap of 0.10%, meaning fees are kept extremely low to maximize long-term growth.

The process to claim the $1,000 seed deposit is straightforward, but there is a timeline to be aware of. To open a Trump Account and claim the $1,000 seed deposit, file IRS Form 4547 with your 2025 tax return or register online at trumpaccounts.gov. The IRS will begin sending account activation information in May 2026, with accounts going live on July 5, 2026.

If you have a child or grandchild born between 2025 and 2028, this is one of those rare moments where doing something small now could have an enormous impact on their financial future. Children born before 2025 will not receive the $1,000 government contribution, but parents can still open accounts for children under 18 and contribute up to $2,500 pre-tax annually on their behalf.

We talk a lot about affordability challenges in the housing market today, and those challenges are real. But the buyers who will feel today’s conditions most acutely are the young people who are still years away from purchasing their first home. Giving them a head start right now, no matter how small it seems today, is one of the most meaningful things we can do for their financial future.

Financial advisors have been saying for decades that early investing is the single most powerful wealth-building tool available to everyday families. A Trump Account is one concrete way to put that principle into action for the children in your life.

Whether you are thinking about buying a home now or planning ahead for the next generation, I am here to help you think through the big picture. If you have questions about how to set your family up for long-term financial success through homeownership, reach out today. Let’s have that conversation.

You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

There is a misconception that floats around every time the Federal Reserve makes a move, and honestly, I get it. The headlines make it sound so straightforward. The Fed cuts rates, mortgage rates go down, buyers rush in, the market opens up. If only it were that simple.

Here’s what I want you to actually understand, because this is the kind of thing that affects whether you make a smart move this year or sit on the sidelines waiting for something that may never arrive the way you expect.

Let me be direct: just because the Federal Reserve lowers its interest rates does not mean your mortgage rate is going to respond the same way. These are two completely different mechanisms, and confusing them leads to a lot of frustration for buyers who keep waiting for a signal that never comes.

The Federal Reserve controls the federal funds rate, which is the rate banks charge each other for overnight loans. The Fed does not directly cut mortgage rates, 10-year Treasury rates, or the rates on corporate debt. Mortgage rates are long-term instruments, and they behave accordingly. Those longer-term borrowing costs tend to move with the 10-year Treasury yield, which rises and falls based on expectations for economic growth and inflation in the years ahead.

So what does that mean in plain language? Even when the Fed is actively cutting, the bond market may be telling a completely different story. And the bond market usually wins.

Here is the part that feels counterintuitive, and it’s one of the most important things to understand right now. A healthy job market is genuinely good news for the economy, but it is not good news for anyone hoping mortgage rates will drop quickly.

Redfin chief economist Daryl Fairweather put it plainly: “Is inflation improving? Is the labor market getting weaker? If the answer to either is yes, then mortgage rates would fall.” That tells you everything. The conditions that bring mortgage rates down tend to be the same conditions that reflect economic pain. The job market hasn’t plummeted like many expected it to, and that’s actually worth celebrating on a human level. But it does mean we are less likely to see the dramatic rate drops some buyers are holding out for.

Redfin’s chief economist noted that inflation will matter more to rates than leadership changes at the Fed or however many short-term rate cuts it makes. “If a new Fed chair cuts rates now, but there’s still inflation, market traders would assume that the Fed will have to increase rates later on to make up for that misstep.” The market is always thinking several moves ahead.

If you want to understand where mortgage rates are headed, stop watching what the Fed announces and start paying attention to inflation expectations. This is where the real action is.

Mortgage rates are heavily influenced by inflation expectations and economic growth. If inflation rises while growth slows, investors often demand higher yields on bonds, which pushes mortgage rates upward. This is one of the reasons good economic news can actually be complicated for buyers. Strong growth and persistent inflation expectations keep rates elevated even when the Fed is in a cutting cycle.

According to Veros Real Estate Solutions’ Q1 2026 update, even if the Fed implements rate cuts, they are expected to be few and not likely to impact mortgage rates in a significant way. The stickiness of inflation in areas like shelter and food is a real factor, and it’s keeping upward pressure on the rates buyers care most about.

Here is the perspective I want you to hold onto, because it matters. Yes, rates are not at 5% and they are probably not getting there anytime soon without some economic turbulence. But we have come a long way.

Since the start of 2023, the average 30-year fixed mortgage interest rate ranged between 5.98% and 7.79%, according to Freddie Mac. As of early March 2026, the latest weekly average 30-year fixed rate reached 6%. That bottom of the range, right around 6%, represents a real improvement for buyers who were staring down 7.5% or higher not that long ago.

The 30-year fixed-rate mortgage averaged 6.11% as of March 12, 2026, according to Freddie Mac. Is it the rate anyone dreamed about during the pandemic? No. But for borrowers with strong credit, the lowest weekly offers tracked by Bankrate were running around 5.6% as of early 2026. The rate you see in a headline is rarely the rate you will actually get, especially if you have prepared well.

The buyers and sellers I work with who are winning right now are the ones who have stopped waiting for a perfect headline and started working with the actual market in front of them.

Rebekah Scott, director of investment real estate at Atlas Real Estate, said it well: “Don’t try to time the bottom. If you find a home that works and a rate near 6%, that’s a solid position by any historical standard.” That is exactly the conversation I have with my clients. Waiting for rates to drop into the 5s could mean sitting out another full year or more while home prices quietly continue to move.

Overall, 2026 is shaping up to be a mild improvement over 2025. Assuming all goes as expected, buyers will gain slightly more purchasing power due to lower mortgage rates, and sellers won’t see a significant decline in home prices. That is a reasonable foundation to work from.

The misunderstanding that any positive economic news equals lower rates has cost a lot of buyers time and opportunity. The relationship is more nuanced than that, and honestly, having someone in your corner who understands the difference can change the whole outcome of your home search.

If you have been waiting on the sidelines trying to make sense of economic headlines, let’s talk. I help buyers and sellers cut through the noise and make decisions grounded in what is actually happening in the market, not what the news cycle wants you to believe. Reach out today and let’s figure out what the right next step looks like for you.

If you have any real estate needs, I’m the realtor for you! You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!

There is a new federal anti‑money laundering rule that directly targets certain all‑cash and non‑financed home purchases, and it is now in effect. The rule is aimed at stopping bad actors from hiding illegal money in residential real estate, especially when properties are bought through entities or trusts with no traditional financing.

This matters for regular buyers and sellers too, because it changes what has to be disclosed and who will be willing to do all‑cash deals going forward.

The rule mainly applies when a residential home is bought without a traditional bank loan and the buyer is a legal entity or a trust, not an individual using their own name. Think LLCs, corporations, partnerships or trusts buying houses, condos or similar residential properties with cash, hard money or private money.

These kinds of deals were often used for privacy or asset protection, but they are now treated as reportable events that must be documented for the U.S. Treasury’s Financial Crimes Enforcement Network, also known as FinCEN.

Under the new rule, a closing or settlement agent, usually the title company or closing attorney, must collect detailed information on the “beneficial owners” behind the entity or trust and submit a Real Estate Report to FinCEN within a set time after closing. This includes names, addresses, Social Security or taxpayer identification numbers and other identifying details for the real people who ultimately own or control the buying entity.

Although real estate agents are not the ones filing the reports, NAR is stressing that we need to understand the rule so we can prepare our clients and avoid last‑minute surprises at the closing table.

For sellers, this rule may reduce some of the looser, more anonymous cash investor activity that has been present in certain markets.

Some all‑cash buyers who used entities or trusts mainly for secrecy may now think twice if they have to reveal their ownership details to a federal database, even if they are not doing anything wrong.

That could mean slightly fewer “mystery” cash offers, but it may also shift the buyer pool toward more transparent, well‑documented purchasers who are comfortable providing their information.

If you are a legitimate buyer planning to purchase with cash through an LLC or trust, this rule will probably feel like a hassle at first.

You will need to be clear and organized about where your funds come from and who the true owners are, because title companies and closing attorneys are being told not to close these deals unless all required information has been collected.

It is easy to feel like you are “under investigation,” even when you are simply trying to buy a home for privacy or estate planning reasons, and that emotional piece is important to acknowledge.

Many buyers have used entities or trusts to keep their names out of public records for reasons like safety, high‑profile jobs or estate planning.

The government is not banning this, but it is saying, “If you are buying non‑financed residential property this way, we still need to know who you are behind the scenes.” Some legal and tax professionals are already outlining compliant structures that balance privacy with the new reporting requirements, but they all come with more documentation and planning than before.

FinCEN has been clear about its main concern. Criminal organizations, corrupt officials and other bad actors often use all‑cash purchases through shell companies or trusts to move and hide illegal money, especially when there is no bank involved to run anti‑money‑laundering checks.

The agency estimates that hundreds of thousands of transactions a year fall into this non‑financed residential category, and they see it as a major weak spot in the financial crime system.

By creating a secure, non‑public database that tracks real owners on these deals, FinCEN hopes to deter abuse and make it easier to follow the money when something looks suspicious.

In practice, this rule adds steps, questions and paperwork for everyone involved in affected cash deals.

Closing and settlement agents now have new forms to complete, new deadlines to meet and new risks if they get the reporting wrong or close without all of the required data.

For buyers, especially those using business entities or trusts, it means gathering personal information for each beneficial owner early, sharing it with the closing team and understanding that your transaction is now part of a federal reporting system, even if none of that shows up in public records.

If you are thinking of buying with cash, especially through an entity or trust, the key is not to panic, but to prepare. This rule does not say cash is bad or that entities are illegal. It says, “We need transparency about who is behind the money.”

Going in with the right expectations, your ownership structure clearly planned and your documents organized can turn this from a last‑minute crisis into just another box you check on the way to owning a home or investment property.

If you are a seller wondering how this might impact the cash buyers who show up on your listing, or a buyer planning to purchase with cash through an LLC or trust, let’s talk before you get too far into the process. I can help you understand how this new rule fits into your specific situation, coordinate early with your title company or closing attorney, and connect you with legal and tax professionals so you can stay compliant while still moving forward with your real estate goals.

If you have any real estate needs, I’m the realtor for you! You can always reach me at tracyYchan@gmail.com or my cell at 973-476-8097.

If you haven’t already, remember to subscribe to our newsletter and get real estate updates in your inbox!